Supreme Courts and Supreme Leaders

In this latest episode, we discuss the SC tariff ruling (with revisit to Trump’s attempt to kill all the lawyers), plus the imminent and inevitable economic collapse: will it be a repeat of the 1970’s energy crisis or a repeat of the 2008 credit crisis? And of course, more music!

Timing is Everything

I was definitely happy I finished the last newsletter just a few days before the Supreme Court invalidated the majority of Trump’s Liberation Day Tariffs and news of Blue Owl stopping normal redemptions at one of their private credit funds. Of course, the timing was not due to any predictive power of mine. You can tell because I didn’t predict the Iran war erupting just week or so later (unlike some others, who predicted the outbreak of hostilities and parlayed that into some significant winnings, as you’ve probably heard about). If I had, I would have rushed to get my prediction market bonus newsletter out (as well as perhaps placing some timely bets myself!). At the risk of missing some fast breaking news, I will nonetheless provide a few minor updates to some of the stories mentioned in the last newsletter. First, JPM finally confirmed that the Trump de-banking was a direct response to January 6th attack on the Capitol (which makes their lobbying on the CLARITY act even more impressive). Second, despite my complaint [or maybe further evidence of the problem] that the home insurance crisis is simultaneously both well-known and completely ignored, articles (including in Australian publications) continue to pop up highlighting the impact of the insurance crisis in the US, including a great opinion piece noting that the insurance crisis is turning people socialist (which I found funny both because (i) insurance is inherently socialist and (ii) apparently political leanings didn’t really change the survey responses (i.e. both R & D voters were equally likely to support things like capping premium increases or making insurance optional)). Elsewhere, in Hawaii, legislators are entertaining the idea of blaming (and charging) the oil industry for the insurance crisis; at the same time, the oil/oil-shipping industry faces its own insurance crisis for tankers trying to navigate through the Strait of Hormuz). But we will talk about that below. But first, the Supreme Court invalidated (some) tariffs!

Supreme Cautiousness

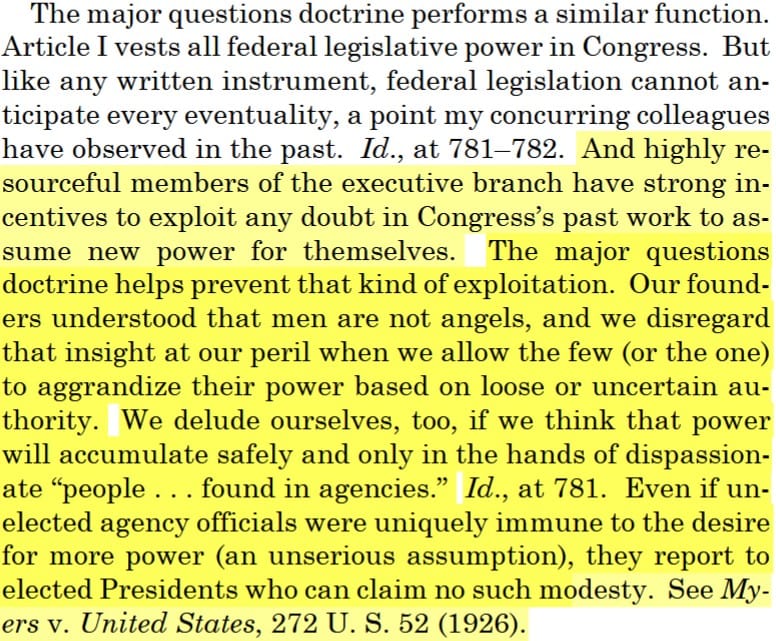

You all saw that the Supreme Court invalidated Trump’s tariffs. And some of you may have read the actual opinion (although, with the exception of Gorsuch’s concurrence, they weren’t necessarily the most fun reads). I think the most important part of the majority opinion was the enormous unanswered question of whether the tariffs will be refunded and how soon (and to whom). Obviously, Supreme Court jurisprudence often tries to answer only the most narrow question possible (an interpretative approach that is not without firm and sensible grounding), but the Supreme Court must have known that the President would not rush to comply with their ruling (has he ever?) and that the administration would likely drag their feet and/or extensively litigate the process of refunds. After all, the enormous amount of money at stake has significant implications for the federal budget and, correspondingly, the success of Trump’s economic plan to cut more taxes for the wealthy [I am guessing here, I thought he also wanted inflation to go down...but the Iran war has me confused on that point]. Moreover, the optics of the Secretary of Commerce’s former [and future, I presume] employer potentially collecting millions of tariff refunds purchased for cheap is a pretty bad look. If John Roberts is concerned about his legacy (and the reputation of the Court), I’d suggest that purposely staying quiet and implicitly allowing further litigation (while making the most passive critiques) and increased gamesmanship around refunding tariffs (a delay which is in fact perpetuating the fiscal impact of the tariffs) by the Trump administration will cover neither Roberts nor the Court in glory. I did, however, very much enjoy Gorsuch’s concurrence, particularly his admonition highlighted below.

In any event, despite the Supreme Court’s cautiousness, the President did not handle the defeat with his normal equanimity, immediately announcing 10% replacement tariffs, and then changing that the next morning to 15% tariffs (both under a separate statutory authority, which may well be unconstitutional as well, by the way). And since things haven’t been going great over at the President’s DOJ, it’s definitely conceivable that he was just very, very angry at both (i) his tariffs being struck down by the Supreme Court and (ii) the shockingly poor management of the release [partial release?] and redaction [attempted redaction?] of the Epstein files.

Killing All the Lawyers:

His frustration also might explain another (humorous) development involving the President’s DOJ and a callback to a topic discussed a few times in previous newsletters (the ones I haven’t yet uploaded to this new platform ☹️), namely the President’s attempt to bully many of the country’s most prestigious law firms with blatantly unconstitutional executive orders. Horrifyingly enough, that only happened only about a year ago, although it certainly feels much longer! But this newest development indicates that we have finally reached the “farce” stage of this dreadful bit of political theater. Why? Well, because after several resounding defeats at the district court level, the DOJ announced that they were dropping any further appeals, acknowledging that these executive orders were unconstitutional (and dismissing the cases). Except! As soon as Trump was made aware that the appeals were being dropped, he called the DOJ and instructed them to re-instate the appeals (which may not even be possible!). Surprising to see such impetuous behavior from an otherwise calm, thoughtful and strategic executive. And that, dear reader, is not political commentary, but rather our humorous segue to the discussion of the Iran war and the economic implications of the calm, thoughtful, and strategic approach we have taken with respect to Iran. Because this is an apolitical newsletter, of course!

Iran War (or Mission Accomplished Part Deux)

Now I obviously don’t remember it (not having been born) but the financial/economic concern arising out of the Iran war turns on whether Iran can (and will) block the Strait of Hormuz (or otherwise destroy sufficient oil infrastructure in its neighboring countries) to bring about another 1970s style energy crisis. As the 1970s were not exactly the best economic period in our nation’s history (or the world’s history, really), distinguished by high inflation and high unemployment (also referred to as stagflation, which you probably have seen bandied about recently). I think it is too early to tell primarily because (as I hinted at in my segue above) it is not clear that this war is part of a comprehensive strategy (as opposed to an impetuous lashing out, or worse, being dragged into a war by an ally who is likely motivated primarily by their own internal political considerations). But probably I should back up and explain why you are seeing stagflation all over the news, coupled with alarmist headlines that “there is no limit on how high the oil price can go”). In the 1970s, the US experienced stagflation - meaning the economy weakened (i.e. the labor market sputtered and worker’s earnings declined) but inflation (the rate of increases in prices) increased and/or continued, which is as unpleasant as it sounds. And although one factor is almost never completely to blame for economy-wide impacts like stagflation (for example, see the Nixon Shock of 1971), the OPEC oil embargo of 1973 (which was a response to the US support of Isreal in the Yom Kippur War) did, in fact, quadruple the price of oil in just a few short months ($3 in October of ’73 to $12 by January of ’74), with consequences which rippled through western economies for years to follow and helped create the stagflationary environment. So, here we are 50ish years later, the US is supporting [following?] Netanyahu’s war against Iran, and it is estimated ~20% of oil flows through the Strait of Hormuz, which may be subject to Iranian drone attacks at any moment. And people are rightly concerned when they see that the ripple of economic consequences have begun without even a viral video of a burning supermax oil tanker – why? because the insurance companies have canceled policies and shipping companies are simply not sending tankers through the Strait. So gas/diesel prices in the US are spiking as are LNG prices in Europe (and not just due to a potential “oil embargo” via closure of the Strait, as the Iranians have also targeted oil infrastructure across the Middle East). So the financial media at least is quickly rolling out articles…”Are we headed for a repeat of stagflation? And can we do anything as personal investors to protect ourselves, if we are headed that direction? Find out after the break!”

Most financial media would have slipped an ad in there, hoping those provocative questions kept you reading and scrolling past the advertisement! Because that is the game in financial media, even when they rarely have good advice or a satisfying answer. [[For example, see this article where the advice to “protect against AI” is to diversify your investments. Yeah, great, thanks, I’d never heard of diversification before.]] If I depended on getting eyeballs to pay my bills [and not my partner’s hard work taking care of veterans in the ER, which is you know, just a hypothetical!!!!], I’d probably have to do the same - i.e. keep you scared about the implications of stagflation, feed you some ads, and then throw in some boring and general financial advice. But I am not worried, don't like selling ads and I certainly don’t want to scare you (or worse, bore you!). I think it is way too early to be concerned or even contemplating changing your investments in any material way. Right now, I think the most important things to remember are: (i) the TACO (Trump Always Chickens Out) trade has not failed us yet, (ii) to replicate the oil shock of 1973, we would need oil prices to skyrocket to something like $300/bbl (FYI - Brent Crude was at ~$73/bbl before the strikes in late February spiked recently to almost ~$120/bbl but is back down below $100/bbl as I type this line), and (iii) our economy is much, much less dependent on oil than it was in the 1970s. So if you drive a massive gas guzzler, might you face more pain at the pump? Yeah, probably. But for right now, my guess is that long before we start to face structural and/or long-term economic consequences from oil prices Trump will chicken out again, declare victory and move on to something new (Bay of Pigs, Part Deux?). Really, I hope it doesn’t happen before I publish the newsletter. Though I suppose an additional side benefit of ending the war soon is that my tax dollars would no longer go towards mistakenly (and yet still illegally) bombing a girls’ school in Iran and killing 150+ children. [[LATE UPDATE: It was a close call, but I don’t think his comments on March 9 were fully committing to chickening out, but I’m liking my analysis!]].

On the other hand, I admit we can’t really be too sanguine about these threats because we really don’t know what the strategic end goal might be (or when it will be created ex post facto). If the Isreali and US strikes ultimately result in a failed state, then it is true that we might see a wider regional conflagration, and the end of cheap oil from the Middle East for a good long time (with the Afghanistan experience potentially being a good example of “a good long time”, and to be clear, I am starting the clock back when the Russians invaded in 1979 and it is still running!). But achieving total regime collapse will likely require something more extensive than air strikes, and it’s hard to imagine there is an appetite for significant boots on the ground in Iran when the US is acting basically unilaterally with (i) a President who ran on no new foreign wars, (ii) a Secretary of War who somehow continues to reach new lows (lethality maxxing, ugh 😦), and (iii) a voting base which cares a lot about gas prices. So, ultimately, I think we will see some sort of resolution (or significant de-escalation) sooner rather than later – and thus any increase in oil prices won’t lead to stagflation or a 1970’s oil shock (even if they don’t revert back to pre-March levels). But, of course, that doesn’t mean the stock market won’t see some significant volatility in the near to medium term. After all, there are a lot of other things going on (AI, Tariffs, potential credit crisis, etc.) which are all concerning to some extent – but it does mean that your investment decisions shouldn’t be overly influenced by the fact that Secretary of Defense War prefers war, rather than thinking strategically about how to defend US interests both here and abroad. Funny how those naming conventions work, I guess. Speaking of names - we do indeed have a sidebar on strait vs. straight (as I am sure some of you were expecting) and a short musical interlude before we get to the looming credit crisis!

Dire Straits, of course! For some amazing guitar from Mark Knopfler!

Private Credit Collapse?!?!?!

No, no – I promised I wouldn’t be alarmist! And previous readers know that I am no fan of the private credit industry (or more specifically) the incipient attempts to make private debt/credit and equity more accessible to individual investors. But still, I am skeptical that these “cockroaches” (as Jamie Dimon refers to them) that we are seeing in the credit market are going to somehow precipitate a repeat of 2008. And it is true that more cockroaches are popping up: besides the Blue Owl news, some other near term warning signs in the private credit market include Blackrock (a couple of times) and MFS going bankrupt in London. But none of this drama in the private credit market will likely affect the typical individual investor (in large part because most individual investors don’t have exposure to these types of funds yet, thankfully; note that Blackrock's limit on redemptions applies to billionaires). Although it does helpfully provide some additional real world examples of why you shouldn’t feel the need to invest in any private credit funds or private equity funds or BDCs or whatever other alternative asset that someone tries to sell you. (Though I suppose I am obligated to caveat that line by saying everyone’s situation is distinct, and this isn’t financial advice, blah, blah, blah, etc.).

If you are taking financial advice from this newsletter (instead of just enjoying the musical interludes and laughing chuckling smiling at the ridiculousness of our financial world), I’d note that this is also a great example of why I support keeping your investments as simple as possible. Because, really, who has time to vet the particular Blue Owl fund they are invested in (what with the episodes of Bluey blaring in the background) and then form an opinion on whether the managers are performing appropriate due diligence on the syndicated loans they are buying for that fund? I know one person who doesn’t have time! And unfortunately, it is my favorite financial columnist, Matt Levine, as exhibited by his embarrassing disclosure about Blue Owl, to wit: “Disclosure: Through a financial adviser, I have a small amount of money in a Blue Owl fund, though I am not sure which one.” So, this is the first (and probably last time) I can smugly look down on Matt Levine by specifically noting that I do not own any Blue Owl (or Blackrock, or any private credit) fund!

Finally, if we are talking about financial advice, I would be remiss if I did not flag – particularly for those readers with children – the story about Mr. Beast getting into the banking business to help provide financial advice to children. It’s quite a story (though if you don’t know who Mr. Beast is, maybe don’t bother trying to catch up) with my favorite part probably being Mr. Beast explaining that he learned about compound interest [which I like] by playing Call of Duty [which I did too much of during law school] and that led to him purchasing/investing in NFTs [which I abhor and do not understand]. Perhaps a more astute (or younger?) reader can help me connect those dots? Anyway parents, don’t let your kids participate in Mr. Beast’s gamification of finance (at least for any of their or your, retirement or educational funds). Teach them to invest in diversified index funds and ETFs, and then they can play games on the side (or apparently, they can become a millionaire through Roblox, which is far from the worst thing your child could be doing online to make money). I will note that one of the creators quoted in that article may have a better concept of compound interest than Mr. Beast, as he notes that his plan is to “just make money from money, and work for fun”. Yup, I think he has it figured out!

For our musical finale, don’t worry, it is not about video games (since I couldn’t think of a good one). Instead, I was concerned that all this talk about war and tariffs and credit collapses and dying Blue Owls might be having you feel a bit blue. So I felt it was better to gamify our last musical interlude and let you choose-your-own-adventure (in a sense) with three songs and three different sorts of blues.

1) Blues Run the Game – a great song by the under-appreciated Jackson C. Frank (but it was also covered by Simon and Garfunkel). I’d say this is the saddest one, except that it always brings a smile to my face to hear lines like “send out for whiskey, baby, send out for gin, me and room service, honey, me and room service babe, well we’re livin’ a life of sin”.

2) Workingman Blues #2 – One of Dylan’s piano masterpieces and also oddly topical for a financial newsletter. And I mean, really, crazily specific. Who would have thought the commentary “the buying power of the proletariat has gone down/ money is getting shallow and weak/ where the place I love best is a sweet memory/ it’s a new path that we trod/ they say low wages are reality/ if we want to compete abroad” would be in the musical interlude, and not in our Communist Corner (which is not actually a repeated theme of the newsletter – despite some readers probably wishing it were!!)

3) Backlash Blues – This is Nina Simone at her most powerful – and, unsurprisingly, she’s not pulling any punches! “You give me second class homes/ And second class schools/ Do you think that all colored folks/ Are just second class fools”. But it’s also just a great blues song.

Pick your favorite – I couldn’t which is why there were three – but maybe you can 😊! And yes, of course my algorithm is secretly tracking which one you prefer so I can better target you with my future missives. Stop whining, you luddite!