New Year, New Newsletter, but the same old news....

In this slightly delayed episode, we do a little forecasting, we talk about hedging and re-balancing, and we spend a bit of time navel-gazing (by “updating you” on some topics which we wrote about a few times in the past year).

Forecasting and Predicting:

No, we’re not forecasting world events (War with Greenland!) or predicting S&P500 prices because as everyone knows, it’s a bit of a fool's errand. And if you wanted to, you’ve been able to read plenty of forecasts already. After all, each January (sometimes starting in December) every magazine, newspaper, blog, website, etc. releases some sort of prediction or set of predictions for the new year. The good ones, of course, go back and revisit their predictions from last year and (typically) find them lacking, unless they were suitably vague that they can argue they should get half-credit. The more disingenuous ones refer back to their “year-end” market predictions which they updated at some point in time in the year. And though I won’t waste your time now with predictions; but I am going to release a bonus newsletter about predictions and prediction markets because I do like the idea of talking about prediction markets and how they are evolving in the world and what, if anything, we can learn from them. So keep your eyes peeled for that. But, no I don’t think anyone is accepting bets as to when it will be out or whether Cardi B will be featured!

But, in this episode of the newsletter, I am forecasting (or maybe just hopefully planning) how the newsletter will evolve this year! Which is publishing (i) slightly shorter monthly newsletters (or monthly newsletters with more and shorter topics) and (ii) more frequent bonus newsletters where the deeper dives on bigger issues will be addressed. And I do appreciate the encouragement from a number of readers who have noted that they enjoy the newsletter and find it both useful and entertaining; so you can rest assured that the style won’t change because entertaining is [of course] what I'm mainly aiming for! But could there be room for improvements in usefulness? Sure – and I’ll be incorporating a few more thoughts about things which are happening and how we might want to interpret those events [to the extent there is anything useful for our financial lives in the news - which is sometimes still going to be pretty tricky].

Hedging:

So, are you invested in commodities as a hedge? I am thinking gold and silver, primarily, since those prices have skyrocketed recently, but also maybe oil, given the geopolitical turmoil caused by our short war with Venezuela in January (Remind me, is that still going on? Were the troops sent to Greenland instead? Is ICE is pulling out of the War in Minneapolis to go down to Venezuela? Hard to keep track!) If so, did you sell “at the top” of the silver market? Are you slowly rebalancing away from your gold holdings? Or are you doubling down on silver because the dollar is going to zero because (i) hard currency is the only future and (ii) you shall not crucify mankind upon a cross of gold!

If you aren’t, however, it really calls into the question why you are holding gold/silver (or other commodity) in your portfolio. Rebalancing is a key part of long-term portfolio management. And if gold has skyrocketed, then you should be reducing your gold holdings because (presumably) the gold holdings have grown faster than your other holdings. If all your holdings have grown (or fallen) at the same speed, of course, it wasn’t a hedge at all (e.g. the correlation was too high). But if it was a hedge (or you incorporated it into your portfolio as a hedge), then congratulations – the hedge (whether gold/silver/etc.) has served its purpose! For example if your gold percentage has gone from 10% to 20%, you should sell some of that gold to get back to the 10% allocation.

Not that I recommend 10% gold as a general matter, although I’ll note that Ray Dalio has an “all-weather portfolio” where with gold at 7.5% and other commodities at 7.5%. [FYI – you may note that he doesn’t have any “digital gold” (i.e. BTC) because, undoubtedly, he noted the correlation with tech stocks; and good thing, since as physical gold has been going up, digital gold has been plunging.] And despite the fact that I don’t use that portfolio myself, I can understand the approach – my real point is merely if your rationale is that it is a hedge then you have to rebalance when it has hedged! And if it is NOT a hedge, then it probably makes sense to be more open about that – it’s more of a speculative move! Which is fine! Although, of course, we (humans) are not very good at speculative investing generally. That's why if you are holding commodities as a hedge in your overall portfolio then you really should be thinking about rebalancing sooner! And, a late update (as various SEC filings come out) is that, in fact, many family offices and large holders did, in fact, trim their metals holdings as those commodities surged! And, as always, if you (i) are impressed with my analysis and (ii) find yourself in need of someone to run your family office since your previous family office CEO held all of your silver positions right through the crash, well…make me an offer I can’t refuse 😊!

But, assuming that won't happen, I'll try and move on to the navel-gazing (by the way, the pejorative term navel-gazing, for the curious, comes from critiques of the Hesychasts, which [I am sure you all recall] were the 13th century order of monks from the Eastern/Greek Orthodox Church who fixed their eyes on “the middle of the body” in order to “attach the prayer to their breathing", which is why the etymology of the term comes from the Greek words omphalos (which, in turn comes from the Omphalos of Delphi and skepsis (meaning investigation, and from whence comes the philosophy of Scepticism), instead of other eastern languages/traditions where inward looking meditation and focusing on your breathing is more common (e.g. various Yoga practices and Hindu traditions). But we should get back to finance and the same old news, although I can't do that without ensuring readers can learn the real lesson of Silver and Gold from the Queen of Country (and amazing philanthropist, particularly for those of you with children learning to read) in our first musical interlude…

Private Equity/Private Debt/Insurance Markets:

There have been lots of articles recently about how PE hasn’t exactly been working out; even though it wasn’t that long ago that everyone wanted to incorporate PE and Private Debt into individual investors 401(k)s (see Newsletter Episode [ ] and a recent update about a lawyer fighting against it (gift link). Also, note in the NYT article I first linked above how the Carlyle CEO’s prediction for 2025 was “gonna be a banner year;” hmm… I wonder if that prediction had anything to do with trying to sell their PE/Private Debt stakes into the 401(k) market…eh, probably unrelated. And there have been a few articles worrying about home affordability (some actually tying them to increased homeowner’s insurance rates (or in the Guardian’s article, the broken insurance industry) or just calling it all “climate change” (a distinction without a difference). And, exciting news for me, there have actually been a few articles popping up that have combined them! Bloomberg’s big feature on easy money loans (gift link) for house flippers in Florida is the best. Yup, private credit funds making risky loans to new house flippers looking to build in a state where housing affordability is headed the wrong way, in large part because of climate change, is shockingly not working out for individual investors! I hope those doctors and dentists didn’t ALSO have a bunch of “private credit” pitched to them by their financial advisors or by Yieldstreet, which I think still runs ads on NPR’s Marketplace(?), despite their many failures.

Stablecoins:

We've talked about stablecoins in the past a little bit, and you may separately have read about the potential CLARITY Act, which is a seeming priority for the Trump Administration (remember, stablecoins were already partially regulated by last year’s GENIUS Act). One of the provisions of the CLARITY Act focuses even more on stablecoins by creating a new class of “permitted payment stablecoins”, and establishing that issuers of these “permitted payment stablecoins” would be subject to the supervisory authority of the banking regulators! Por fin! Apparently, the hold-up in it passing (or at least some of the hold-up) is about staking, and whether staking rewards (described as “resembling bank interest” by some) will be limited or even prohibited. Coinbase opposes these limitations; the banking industry supports them. Why? Well, the Nasdaq writeup sums stablecoins pretty succinctly, but thereby basically explains the entire issue: “[stablecoins] can be held without a bank account, used for quick overseas transfers, and staked (locked up on a blockchain) to earn interest-like rewards”.

So yeah, stablecoins have always just been bank accounts with “private money”, except with (i) no KYC requirements, (ii) easier/cheaper overseas transfers (eating away at bank transfer fees and avoiding the risk of US government seizure inherent with using a US regulated bank (i.e. almost all of them)) and (iii) holders earn a much higher interest rate than the interest the big banks pay!. But the big banks, though slow moving, have apparently finally aligned their lobbyists to address this threat. And in fact, it appears they may win and protect their business model against stablecoins despite (i) having to deal with the most “crypto-friendly” administration ever and (ii) the fact that some of these big banks decided to cease doing business with Trump administration (for unclear reasons but which almost assuredly involved a number of regulatory concerns in addition to the credit risk caused by the frequent bankruptcies of the Trump businesses). And although I typically find myself complaining about oligarchic industries which engage in unceasing regulatory capture, I have to admit I am with the big banks on this one. I just wish they went further to argue that the US doesn’t need any more or different laws [this is how you can tell I am no longer a practicing lawyer!] merely because a bunch of tech bros wanted to try and reinvent the banking system by calling private bank deposits “stablecoins”. As nearly always, Matt Levine (a much better writer, and another non-practicing lawyer [probably a better lawyer too]), has been writing about this for a long time as well (that last link has a good long example; if you are interested). My take is that we should just call them bank deposits and use the current regulations! (And if that means a lot of the crypto-bros go to prison because they have been violating bank regulations? Oh well. I suspect they’ll get out pretty quickly with some targeted donations!).

Congressional Stock Trading:

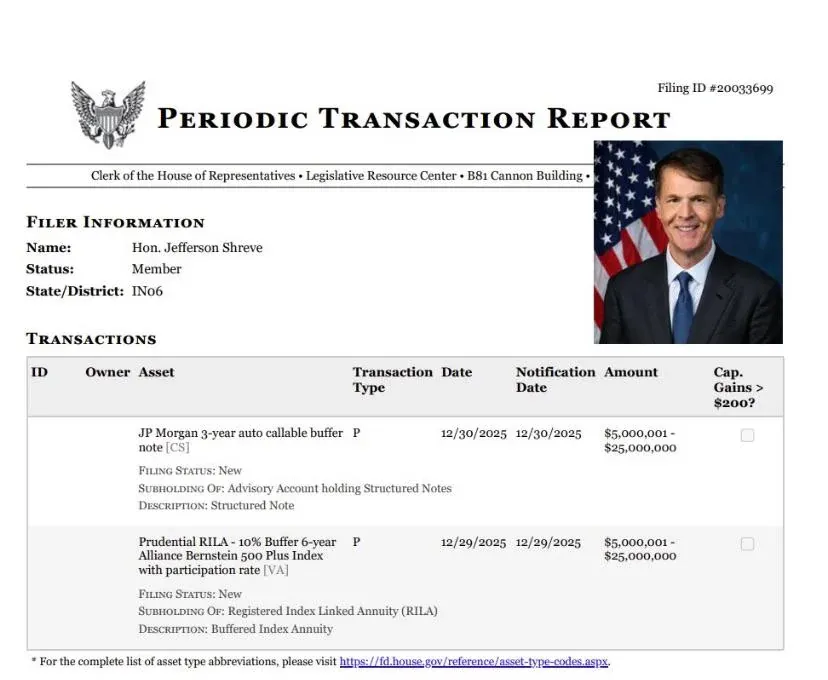

Speaking of politics, I’ll wrap up this shorter (?) newsletter up and move on to my prediction market bonus newsletter (which I am clearly still working on) by returning to congressional stock trading. Now luckily, this particular example isn’t further evidence of the depravity and corruption of our political class (and I think the Epstein saga has provided all of us plenty of that), instead it is a pretty funny periodic transaction report for congressman. As you recall, I’ve complained numerous times about the failure of our government to restrict congressional representatives and their families from trading individual stocks and bonds etc. (mainly to preserve trust in the financial system), but I have also noted that sometimes this might even help these same representatives. I rudely suggested that Rho Khanna (D-California) supported the bad mainly because he was wildly underperforming both Nancy Pelosi (D-Silicon Valle) and the S&P500. I apologize to Rep. Khanna for two reasons: (i) he’s done a commendable job on Epstein and trying to protect democracy and (ii) he could have done way worse, as evidenced by Rep. Shreve (R-Indiana) buying a substantial chunk of both (i) three-year auto callable buffer notes and (ii) “10% Buffer 6-year 500 Plus Index with participation” variable annuity.

Now obviously I have no insight into his financial position (though I note that he is quite wealthy, even for a member of Congress) and there may be some good reasons (almost assuredly tax-related) for these purchases. But typically these sorts of structured notes/variable annuities are really only good for boosting the profits of the big banks/insurance companies which make them [see, I haven’t changed!!!] and the financial advisors which sell them. And they are definitely the type of products which are sold to people; perhaps Rep. Shreve has a very astute financial mind for these things (though he made his fortune primarily through real estate investing/the storage unit industry), but I’d be surprised if he came up with these ideas and pitched them to JPM! I am sure it was his financial advisor selling it to him… so… you know, if I may: [Representative Shreve: we may not share a lot of political similarities but investing advice is apolitical so give me a call. You can trust me because I don’t work in bank]. And yes, I did set up that last line to share the second and final musical interlude, a short but fun little song by Joe Pug (live version below, shorter version above).

But with that, I will wrap this up - and apologize that actually, Rep. Shreve, I can’t take you on right now as it has been a very busy start to the new year here at Fangorn with a number of new clients (in addition to all the regulatory filings!) and so you’ll have to wait! Which means, I guess, that if any one placed bets on Kalshi at the beginning of the newsletter that I would eventually make an excuse for the long delay, well…you won!